It involves calculating the gross profit ratio by dividing the gross profit by net sales. This ratio is then applied to the net sales during the accounting period to estimate the cost of goods sold. Subtracting the estimated cost of goods sold from the cost of goods available for sale gives the estimated ending inventory.

What are the methods of attaching prices to ending inventory?

- However, the portion of the total value allocated to each category changes based on the method chosen.

- The second sale of 180 units consisted of 20 units at $21 per unit and 160 units at $27 per unit for a total second-sale cost of $4,740.

- Regardless of which cost assumption is chosen, recordinginventory sales using the perpetual method involves recording boththe revenue and the cost from the transaction for each individualsale.

- The cost of ending inventory is determined by accounting for the acquisition costs of each item in the ending inventory.

As you’ve learned, the perpetual inventory system is updated continuously to reflect the current status of inventory on an ongoing basis. Modern sales activity commonly uses electronic identifiers—such as bar codes and RFID technology—to account for inventory as it is purchased, monitored, and sold. Specific identification inventory methods also commonly use a manual form of the perpetual system. It has grown since the 1970s alongside the developmentof affordable personal computers. Universal product codes, commonlyknown as UPC barcodes, have advanced inventory management for largeand small retail organizations, allowing real-time inventory countsand reorder capability that increased popularity of the perpetualinventory system. These UPC codes identify specific products butare not specific to the particular batch of goods that wereproduced.

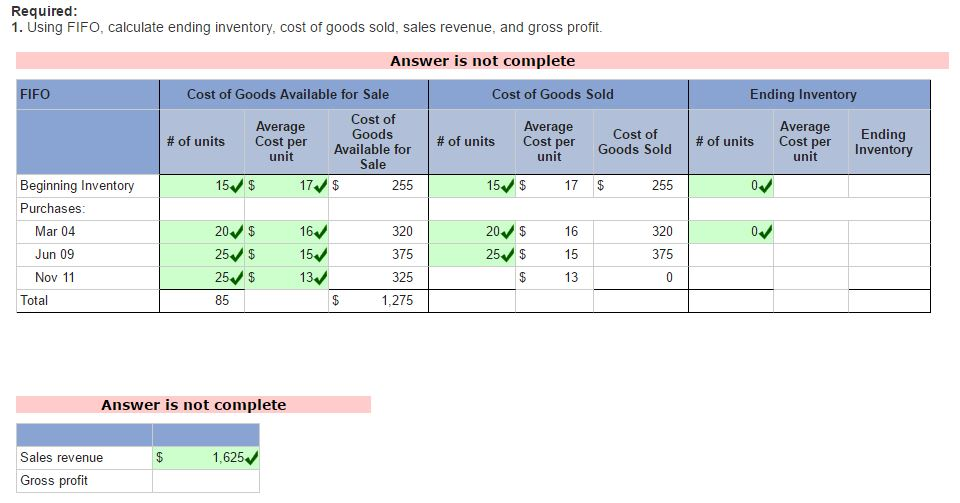

2 Calculate the Cost of Goods Sold and Ending Inventory Using the Periodic Method

Whenapplying perpetual inventory updating, a second entry would be madeat the same time to record the cost of the item based on the AVGcosting assumptions, which would be shifted from merchandiseinventory (an asset) to cost of goods sold (an expense). The LIFO costing assumption tracks inventory items based on lots of goods that are tracked, in the order that they were acquired, so that when they are sold, the latest acquired items are used to offset the revenue from the sale. The following cost of goods sold, inventory, and gross margin were determined from the previously-stated data, particular to LIFO costing. The FIFO costing assumption tracks inventory items based on segments or lots of goods that are tracked, in the order that they were acquired, so that when they are sold, the earliest acquired items are used to offset the revenue from the sale.

Calculations of Costs of Goods Sold, Ending Inventory, and Gross Margin, Specific Identification

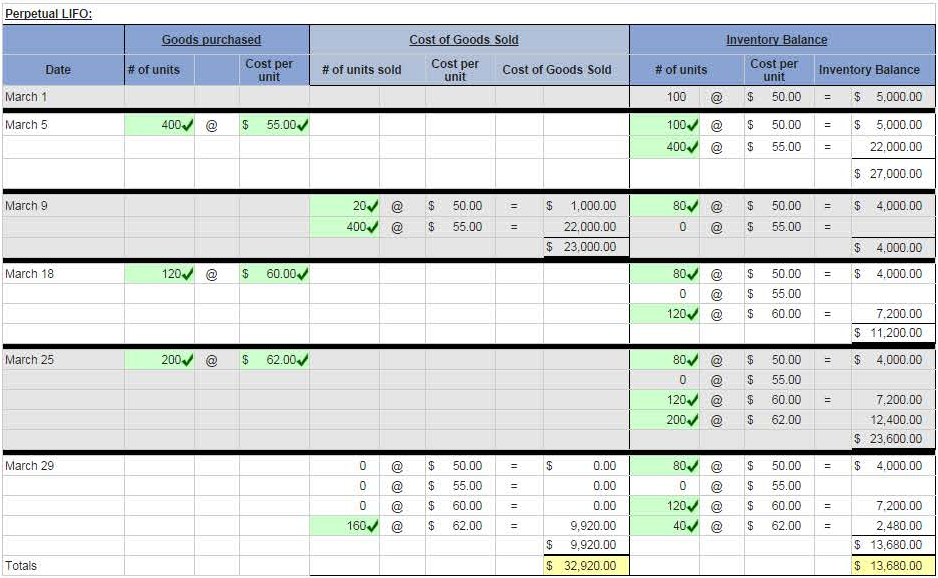

When perpetual methodology is utilized, the cost of goods sold and ending inventory are calculated at the time of each sale rather than at the end of the month. For example, in this case, when the first sale of 150 units is made, inventory will be removed and cost computed as of that date from the beginning inventory. The differences in timing as to when cost of goods sold is calculated can alter the order that costs are sequenced.

Specific Identification Method:

Cost of goods sold was calculated to be $9,360, which should be recorded as an expense. The inventory at period end should be $8,955, requiring an entry to increase merchandise inventory by $5,895. Cost of goods sold was calculated to be $7,200, which should be recorded as an expense. Merchandise inventory, before adjustment, had a balance of $3,150, which was the beginning inventory. The inventory at the end of the period should be $8,895, requiring an entry to increase merchandise inventory by $5,745. Cost of goods sold was calculated to be $7,260, which should be recorded as an expense.

This average cost is then used to assign costs to both the cost of goods sold and the ending inventory. The LIFO method assumes that the inventory items that enter the system last are the first ones to be sold. Consequently, cash vs accrual accounting: whats the difference the costs assigned to the latest units are charged to the cost of goods sold. Under the FIFO method, it is assumed that the inventory items that enter the system first are the first ones to be sold.

It has grown since the 1970s alongside the development of affordable personal computers. Universal product codes, commonly known as UPC barcodes, have advanced inventory management for large and small retail organizations, allowing real-time inventory counts and reorder capability that increased popularity of the perpetual inventory system. These UPC codes identify specific products but are not specific to the particular batch of goods that were produced. Electronic product codes (EPCs) such as radio frequency identifiers (RFIDs) are essentially an evolved version of UPCs in which a chip/identifier is embedded in the EPC code that matches the goods to the actual batch of product that was produced. This more specific information allows better control, greater accountability, increased efficiency, and overall quality monitoring of goods in inventory.

For a firm to calculate the total cost of its ending inventories, it is first necessary to determine the actual quantity of items in the ending inventory and then to attach a price to these items. Figure 10.20 shows the gross margin, resulting from the weighted-average perpetual cost allocations of $7,253. The first step is to figure out how many items were included in COGS and how many are still in inventory at the end of August.

At the time of the second sale of 180 units, the LIFO assumption directs the company to cost out the 180 units from the latest purchased units, which had cost $27 for a total cost on the second sale of $4,860. Thus, after two sales, there remained 30 units of beginning inventory that had cost the company $21 each, plus 45 units of the goods purchased for $27 each. Ending inventory was made up of 30 units at $21 each, 45 units at $27 each, and 210 units at $33 each, for a total LIFO perpetual ending inventory value of $8,775. The specific identification method of cost allocation directlytracks each of the units purchased and costs them out as they aresold. In this demonstration, assume that some sales were made byspecifically tracked goods that are part of a lot, as previouslystated for this method.